Explore and follow profiles from this article to get timely updates:

Late payments among Finnish and Swedish publicly listed companies are rising.

In Finland, payment remarks – negative records on companies' credit reports due to unpaid bills – remain rare and small in scale. In Sweden, they are concentrated in a handful of companies, but at significantly larger levels, pointing to a more fragile underlying risk. Data from Enento Group, analyzed by Listeds, shows that while only a small share of listed companies in both markets have registered payment arrears, the severity and financial implications differ sharply.

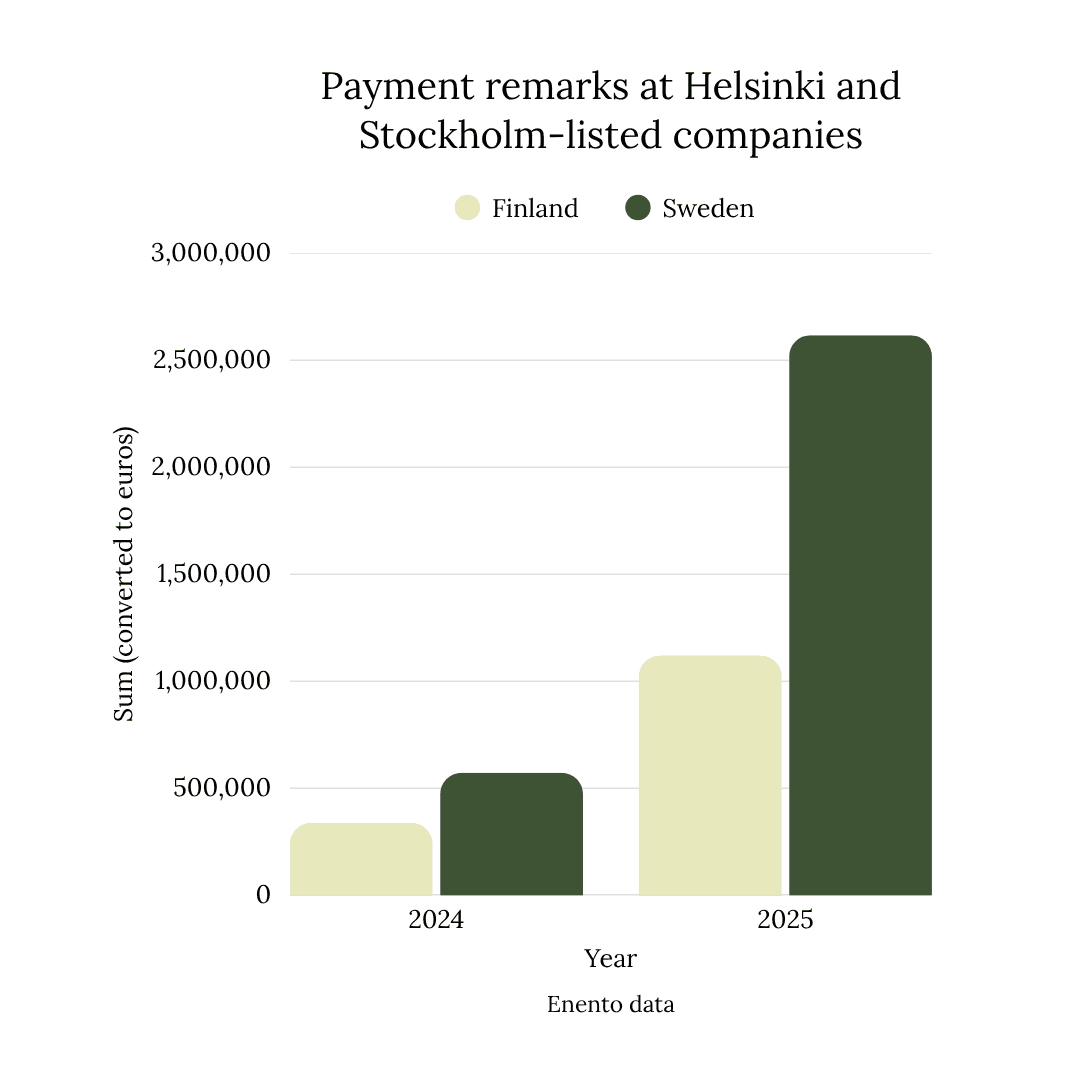

By the end of 2025, 13 of 185 listed companies in Finland, or about 7 percent, had recorded arrears. Total unpaid obligations rose from roughly €0.3 million to €1.1 million over the year. In Sweden, just 15 of 729 companies, or about 2 percent, had arrears, yet the total value increased more sharply, from SEK6.3 million to SEK28.7 million (€572,030 to €2.6 million).

At first glance, Sweden appears more stable, with fewer affected companies across a much larger pool of listed firms. Yet this comparison obscures a more telling contrast. The number of companies in arrears is broadly similar in both countries, but the financial exposure in Sweden is more than double. The issue, then, is less about how many companies fall behind and more about the scale of their obligations.

The rising arrears point to underlying financial distress. In 2025, Finland recorded its highest number of bankruptcies since the 1990s, while Sweden faced record levels of insolvencies, says Pekka Liukkunen, manager of predictive modeling at Enento. The buildup of risk appears to have stabilized early this year; the months ahead will show whether levels begin to decline, he adds.

However, Liukkunen also points to signs of recovery. Both Finland and Sweden have seen a strong number of new market entrants, suggesting potential for renewed growth, he says.

Pekka Liukkunen, manager of predictive modeling at Enento, suggests recovery could be supported by a rising number of new market entrants.

Concentration in both markets, but on a very different scale

In both markets, late payments are highly concentrated. A small number of companies account for nearly all unpaid obligations.

In Finland, the five largest cases make up almost the entire €1.1 million total. These include smaller or mid-sized companies such as Pallas Air, Tecnotree, and Sunborn International, alongside a limited number of larger names. Even among large-cap companies such as Neste, Wärtsilä, Nordea, and Stora Enso, arrears appear but only at minimal levels, typically a few thousand euros. This suggests that, in most cases, late payments in Finland reflect administrative delays rather than deeper financial stress.

Sweden follows the same structural pattern of concentration, but on a very different scale. The five largest cases account for virtually all arrears, pushing the total close to SEK30 million. The companies behind these figures are typically smaller, growth-oriented firms, including TradeDoubler, RightBridge Ventures, Mavshack, Anoto Group, and Adventure Box Technology. Unlike in Finland, arrears in Sweden are measured in millions rather than thousands, and have often increased sharply year on year.

Financial fragility vs operational noise

The financial profiles of these companies reveal a more fragile picture. Many combine weak or negative profitability with low credit ratings, and in some cases operate with limited or even negative equity buffers. Without a sufficient equity cushion, even modest financial pressure can quickly translate into unpaid obligations. Research from the International Monetary Fund has shown that companies reliant on external financing and operating with low profitability are particularly exposed when financial conditions tighten. The Swedish cases align closely with this pattern.

In contrast, companies with arrears in Finland generally retain stronger balance sheets. While profitability may be weaker than peers and credit ratings lower, equity buffers remain intact. This reinforces the view that most Finnish arrears are limited in scope and financial impact, and are more likely linked to timing or administrative factors than structural distress.

A structural market divide

The divergence between the two markets reflects deeper structural differences. Sweden’s equity market includes a larger share of small-cap and growth companies that depend on continuous access to external capital.

Finland’s market, by contrast, is more heavily weighted toward industrial and established companies with stronger balance sheet discipline and more stable cash flows. As financing conditions tighten, these structural differences begin to show up in payment behavior.

A sharper signal for investors

Across Europe, delayed payments are widespread among small and medium-sized enterprises, with more than half reporting related challenges. Among listed companies, however, arrears remain rare, which makes them a more meaningful signal.

What emerges from the Nordic comparison is not a difference in frequency, but in severity and implication. In Finland, arrears are concentrated yet contained, with limited financial impact. In Sweden, they are equally concentrated but significantly larger and more closely tied to financially weaker companies.

For investors and creditors, this distinction is critical. In Finland, late payments with listed companies largely reflect operational noise. In Sweden, they increasingly function as an early warning signal of concentrated financial stress.

Stay on the pulse, catch the signals

Subscribe to Listeds Leadership Intelligence Platform:

leader and company database access

email alerts

career, boards and interim opportunities